Global Securities Firms Regulatory Inquiry App

This week's US non-farm and other major events preview

Last Friday, the core PCE inflation rate released by the US in May increased by 2.6%, reaching a new low in more than three years. This data has lowered the outlook for short-term inflation among US consumers, once causing the US dollar and US bond yields to fall, and increasing market expectations of interest rate cuts. The US stock market generally fell on the last trading day of June, with the S & P 500 Index and Nasdaq Index closing lower after hitting new highs during the day, along with the Dow Jones Index.

This market dynamic may be related to the pessimistic predictions of Goldman Sachs and JPMorgan Chase for the US stock market. Both institutions believe that the expanding fiscal deficit and the high concentration of gains are accumulating risks and are not optimistic about the prospects of the US stock market.

BCA Research's Chief Global Strategist Peter Berezin predicts that based on Friday's Closing Price, the S & P 500 Index may fall by more than 30% this year. This economic downturn may spread from the US stock market and put pressure on global stock markets.

Amazon, Google, and Microsoft's stock prices fell from their highs, while most chip stocks performed well, although Nvidia's stock price rose 3% and then fell 0.4%. In the first half of the year, the artificial intelligence boom pushed the Nasdaq index up 18% and the S & P 500 Index up 14.5%.

Weak consumption is putting pressure on the labor market

Berezin believes that the accelerated slowdown in the labor market will also put pressure on the US stock market. This is because the sluggish labor market also affects consumers' spending power, leading to slow economic operation.

Even if the expected economic recession comes, the US will not immediately cut interest rates because it needs to consider the possibility of inflation restarting; at the same time, the existence of a large fiscal deficit in the US will make the effect of monetary stimulus not necessarily significant.

Michael Pierce, deputy chief US economist at Oxford Economics, also said the weakness in the labour force meant Fed officials needed to focus on risks to full employment.

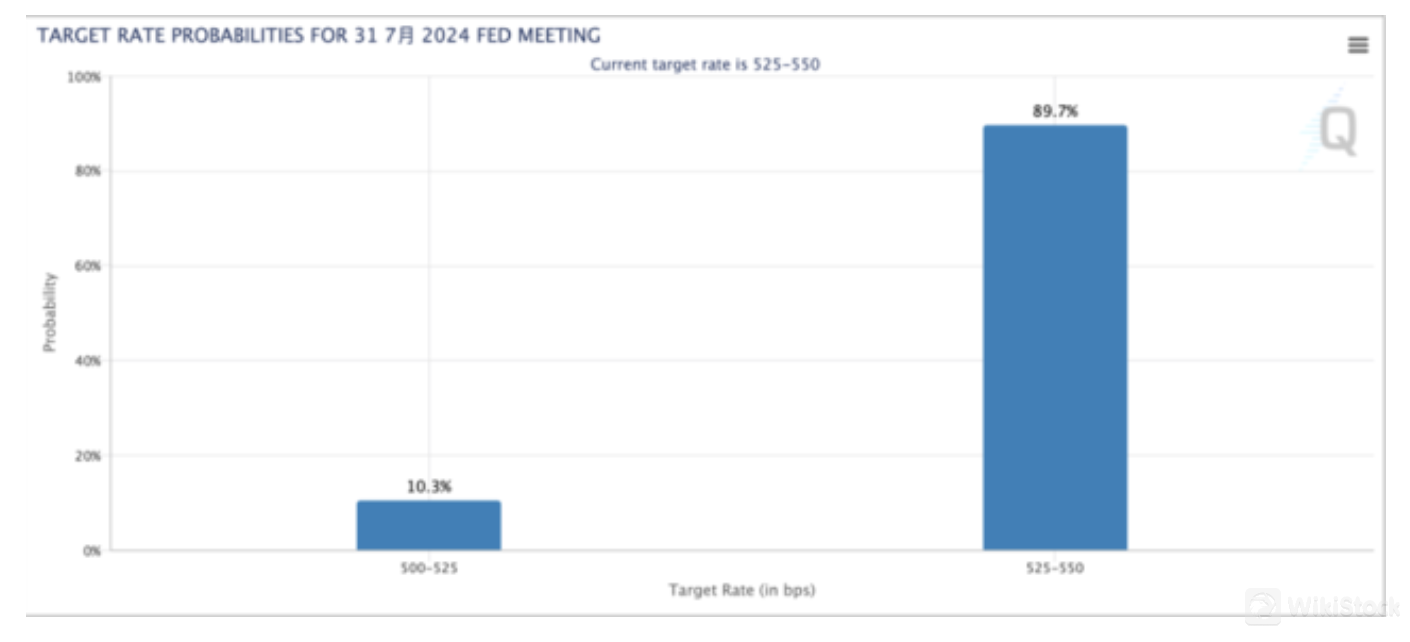

At the June meeting of the Federal Reserve, the Federal Open Market Committee (FOMC) expected to cut interest rates once this year. According to the Fed Watch tool of CME Group, the probability of the Fed cutting interest rates in July is only 10%. It is expected that by September, the probability of the Fed keeping interest rates unchanged is close to 40%. If the latest employment report shows a slowdown in the labor market, investors may increase the possibility of expecting the Fed to cut interest rates.

Image source: Yahoo Finance

Federal Reserve Governor Cook said the current labor market is similar to before the global epidemic broke out and has not exceeded much.

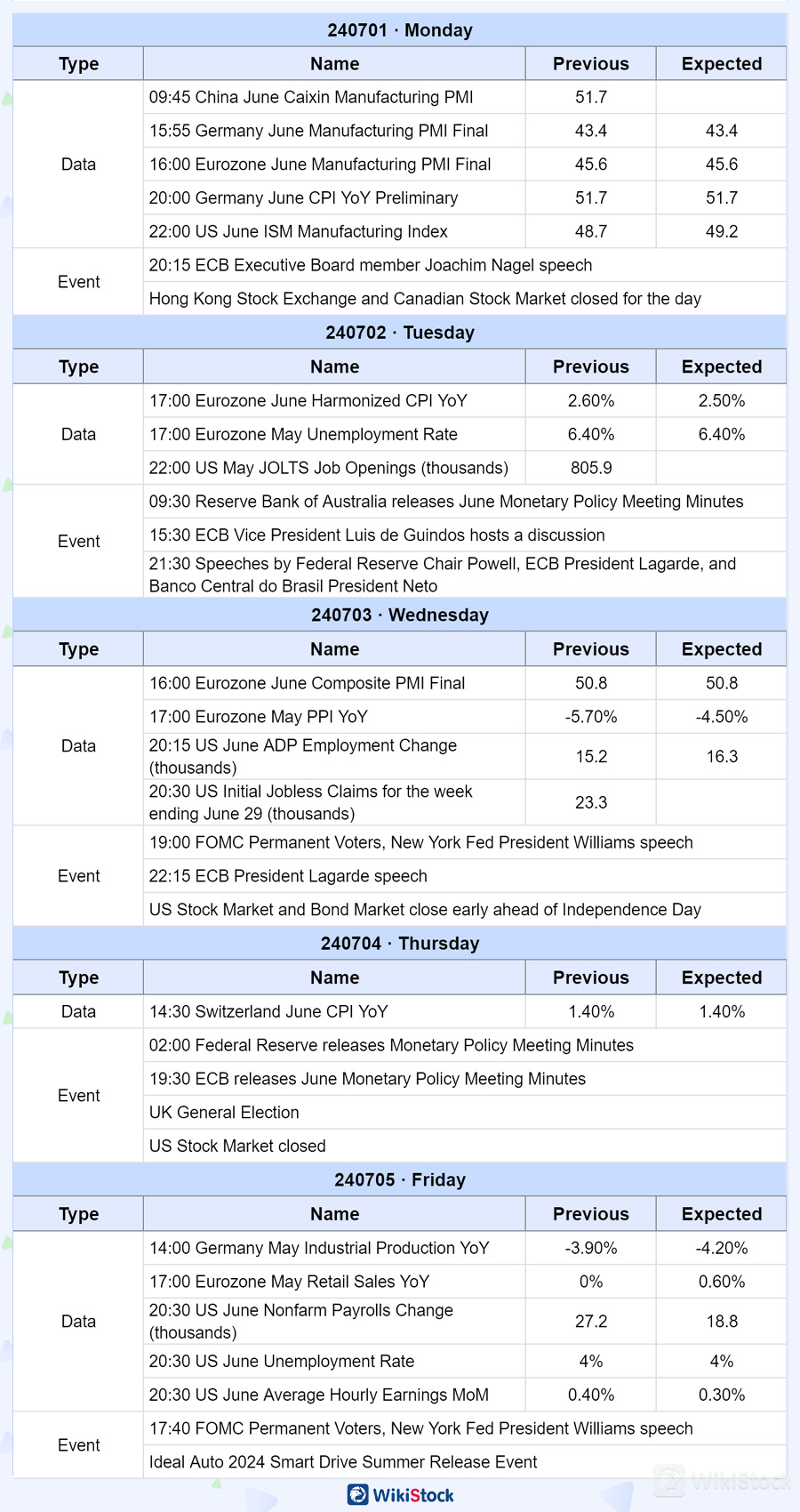

Overview of this week's data

Non-farm payroll data and Federal Reserve speech

On July 5th (this Friday), the US Department of Labor will release non-farm payroll data and unemployment rate data for June.

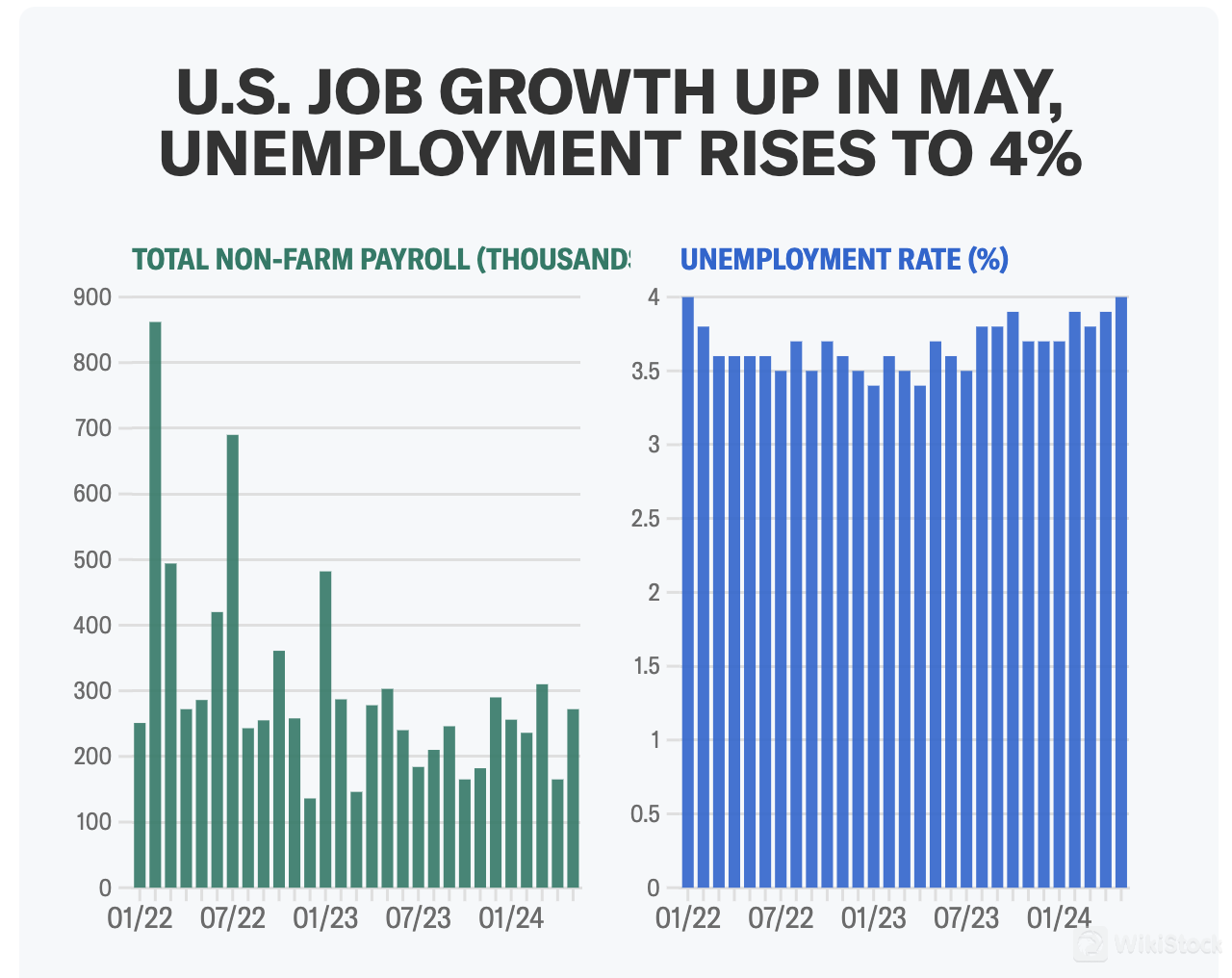

Looking at the May data, the US added 272,000 jobs, leading to a slight increase in the unemployment rate to 4%. Bloomberg predicts that the US added 188,000 non-farm jobs in June, and the unemployment rate will remain unchanged at 4%.

Morgan Stanley's report shows that non-farm employment growth is expected to slow to 210,000 in June, and the unemployment rate will remain at 4.0%. This change is influenced by the dual impact of labor supply and demand, with the decrease in labor supply mainly due to the slowdown in immigration inflows, while the decrease in demand is reflected in the decrease in job vacancies and the increase in new unemployment claims.

Image source: Yahoo Finance

Speech at the European Central Bank Forum

On Tuesday, Federal Reserve Chairperson Jerome Powell, European Central Bank President Christine Lagarde and Brazil's central bank President Benito will speak at the ECB forum.

Recently, major central banks around the world have adjusted their expectations for interest rate cuts again because they are facing more persistent inflation than expected. The wave of interest rate cuts initially expected to start in 2024 did not come as expected, so people are particularly concerned about Powell and Lagarde's statements on inflation and interest rate cuts.

After the Bank of Canada cut interest rates, inflation rebounded. The consumer price index rose by 2.9% year-on-year in May this year, higher than 2.7% in April. The market generally believes that this inflation rebound has increased the uncertainty of whether the Bank of Canada will continue to cut interest rates in July.

Meanwhile, inflation in Australia has also risen, with the weighted consumer price index growing at an annual rate of 4% in May, exceeding the market's consensus expectation of 3.8%. Deutsche Bank predicts that the Reserve Bank of Australia will raise the base rate by 25 basis points to 4.6% in August.

In addition, although the European Central Bank has begun to cut interest rates, Kazimir, a member of the European Central Bank Governing Council, recently stated that the risk of rising inflation is still significant, and another interest rate cut is expected this year.

Other data

This week, multiple countries including China, Germany, France, the European Union, the United Kingdom, and the US will release PMI data. South Korea, Japan, and Germany will release the final manufacturing PMI data for June on Monday, while the US will also release the ISM manufacturing index for June.

This week will also release China's June Caixin PMI data. Previous data showed that China's Caixin manufacturing PMI rose to 51.7 in May, reaching a new high since July 2022; the service PMI was 54, reaching a new high since August 2023.

Byte refutes rumors of speculation on A-share Doubao concept stocks

How to develop a low-altitude economy

Doubao concept surges, IPO economy booms

5G enters the "second half", which stocks are the best to buy

Check whenever you want

WikiStock APP